#23: How to Write a Good Pitch Deck

Over the years, many friends have asked me to review their pitch decks and provide advice before they go out to raise capital. I’ve now been on both sides of the table for long enough — writing decks as a founder, reading decks as an occasional angel — to recognize some patterns that work and some that don’t. There is one piece of advice I received early on in my journey that has stuck with me — I repeat it often — that I want to share with you today. While I discuss this from the perspective of founders raising venture capital, it’s broadly applicable (by analogy) to many other situations where you’re making a pitch. I’ll state it up-front, and then we’ll go into detail:

A good pitch deck makes it easy for the reader to write an investment memo.

Classic advice on writing is to remember your audience, to empathize with your reader, and make your writing accessible to them. In this way, the advice to founders writing pitch decks is to simplify, simplify, simplify — assume the investor doesn’t have much time to read the deck, focus on the key points, etc. This is all true, but it misses what’s next in the process. Keep in mind that the investor wants to learn and understand your company, but they also have work to do: a process to follow, and documents to write. You want to make it easy for them to do their work.

The investor reads your deck, they may take a call with you, and then they may share your deck and their notes with other people on their team. Early on in the process, the notes might be informal, like some bullet points in an email. Later on in the process, they will draft an investment memo to recommend to the rest of their team — and to memorialize for the investors in the fund — why to invest in your company. At that point, you will have supplied many other materials that they may use to write the memo, but the deck is the anchor that people will most frequently refer back to.

When you pitch, you are taking on a process that should result in an investment memo on the other side. This means that two things are very important:

You should know what an investment memo looks like.

You should make it as easy as possible for the investor to draft their memo.

What Does an Investment Memo Look Like?

Depending on the firm, sector, and stage, investment memos have different formats and styles. Thankfully, there are enough public examples1 that you can get a feel for them. Some examples below:

1Confirmation’s memo for Bridge.xyz (2022)

Sequoia’s memo for Youtube (2005)

Canaan’s memo for On24 (1999)

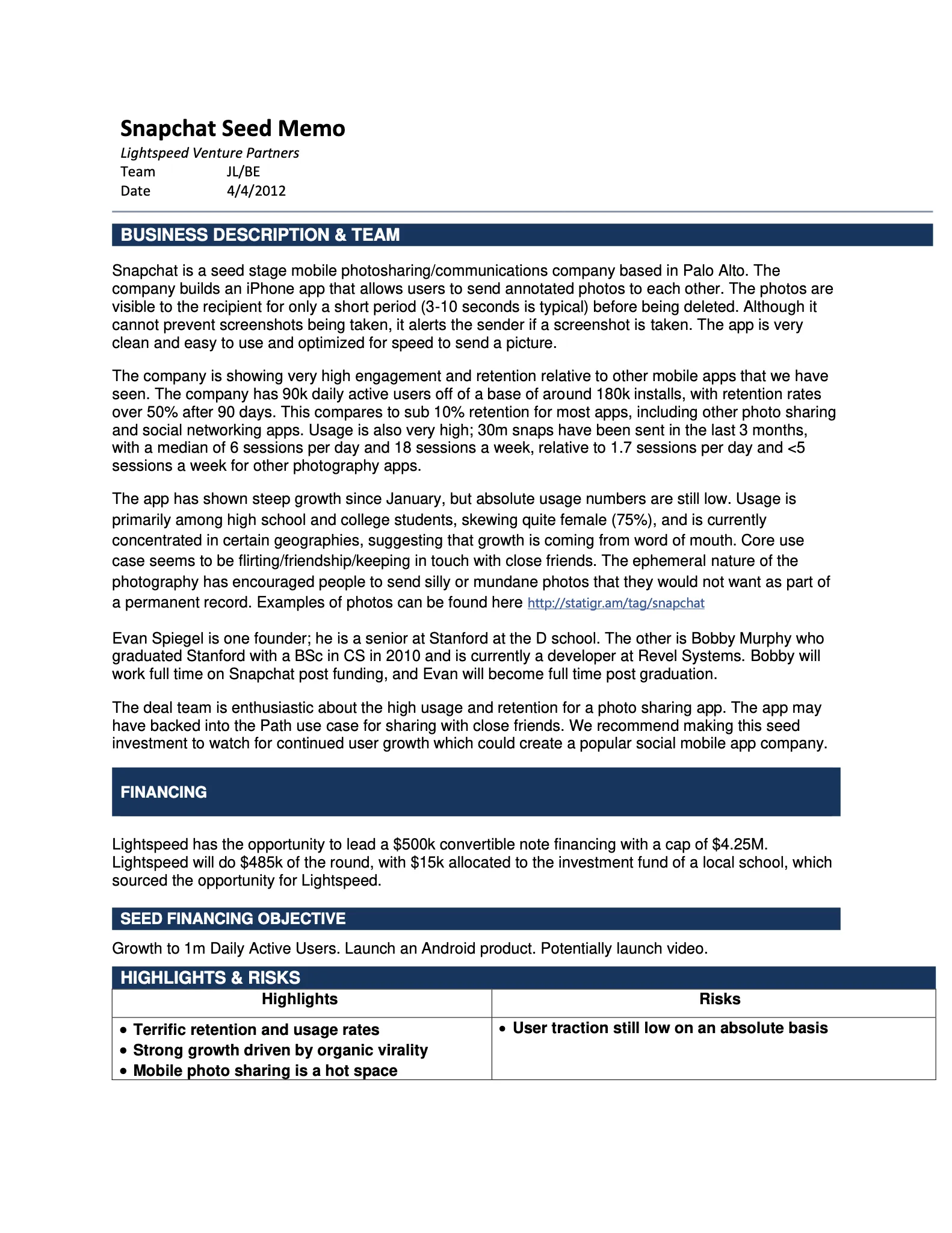

Lightspeed’s memo for Snapchat (2012)

Redpoint’s memo for Ramp (2021)

Greylock’s memo for Roblox (2018)

Bessemer has published 17 memos for investments between 2005 and 2015.

{kind=link}

Additionally, some firms write about their processes and how they draft their memos. NextView has a fine blog post on this, for example. As you dig into these examples, you’ll notice a few things:

Venture firms tend to examine businesses from a different perspective than how a founder might present them — paying a lot of attention to areas that a founder might not, and vice-versa.

Writing a memo is not easy!

It’s a good exercise to try yourself. Write a memo for a company that you’re familiar with. Write a memo for your own company. (One of the underrated benefits of investing in startups is that it gives you more of an investor’s perspective when writing the pitch for your own company.) Having some empathy for and familiarity with the work that happens on the other side will make your presentation of your company much better.

Make it Easy for Them to Write their Memo

I usually recommend the following process. First, put together your pitch deck organically — there are many good templates and structures you can adopt — and present your business however you feel is right. Then examine your deck from the investment memo perspective:

For every slide: are you presenting information in the way that you’d expect it to be reflected in the memo? What would the memo version of the same content say? If there’s a big difference, consider presenting the information another way.

For every piece of information: does it get in the way of the reader as they’re doing their work? Does it distract? If it’s certainly not going to make it into the memo — maybe it’s a detail, but still important — consider moving it to an appendix or a supplementary document.

Are you missing any information that the investor would normally mention in a memo to their colleagues? Include it.

Applying this framing should help take you out of the bubble of your own perspective, and clarify your work. In practical terms, this normally simplifies your pitch, moves content from abstract to concrete, and helps reduce downstream games of telephone as investors try to interpret your work.

Tactics and Pitfalls

Expectations Cascade

Sometimes it’s temping for a founder to skip a slide that an investor might expect, like on TAM, revenue projections, or competition. The founder may have a rational reason for doing so, and write it off as an unnecessary hoop to jump. But the investor knows that their colleagues will want to know those things as they try to understand the business.2 If you don’t provide the information, the investor will have to try to put it together on their own. Usually, you’re better off presenting that information up-front and guiding their research.

Answer the Simple Questions

Try to anticipate the questions that you’re going to get in a slightly adversarial reading of your deck. For example, if you only have a few months of revenue progress and some LOIs, reading that can be confusing for outsiders. I have often had to ask “okay, who are your top five customers, how much are you they paying you this year, and what do you think they will pay you next year?” as I try to wrap my head around what’s going on inside a company. A simple table in the appendix can do wonders.

From another angle: imagine an investor casually bringing up your pitch to their colleagues internally for a gut-check, and answering their basic questions like “what does the company do?” and “why is this interesting?” Your deck should equip the investor with all the key talking points and make it super easy for them to advocate on your behalf, before having spent many hours on a deep-dive.

Use a Supplementary Memo

One of the main challenges in writing a deck is figuring out what’s superfluous and can be struck. Everything feels important! To sidestep this, some founders like to keep their pitch decks brief, and write a comprehensive document as a supplementary memo. Personally, I like that format. It lets you keep the deck as an overview, and gives you a place to put all the details. That document should provide to the investor everything they need to understand your business, and to write their investment memo. (Of course, they will consider many other materials as they do their diligence, but the materials that you provide will always function as the entrypoint.)

Provide Good Resources

As investors dig in on your business, they will want to consult lots of external resources. They will start from your deck (and/or supplementary memo): they’ll look up and double-check the industry statistics you cite, research the competitors you mention, etc. You can make it easier for them by using footnotes in your deck to link to resources they can read. Ideally, a resource that you link to doesn’t just back you up on one particular fact, but generally gives the investor high-quality information that feeds well into the case for your business.

Testimonials

Founders sometimes play coy with the identities of their customers. They might write things like “Amazing product, I’d pay lots of money for this” - Fortune 500 COO in their deck and then voice-over the identity of the person in a live pitch, or provide logos of big customers, but not name who specifically at the firm bought the product. There’s nothing quite as useful for an investor as a discussion with your customers — make it easy! If you’re confident that your customers will provide good testimonials, and they’re willing to act as references, then always provide their names.3

Competitors and Comparables

Founders often focus on competition in their slide decks, trying to point out why what they’re doing is distinct and special. But competition isn’t important in a deck just as a threat to the business, but also as a reference point: for example, your legacy competitors in the public markets are useful to look at, because they show how such businesses are valued at scale, how their market is evolving, whether they might be good acquirers of your company one day, etc. Understanding how to value your business can be nontrivial, and clear enumeration of the comps will, just like everything else in this essay, save the investor time as they dig in on your business.

Conclusion

If you want to work productively with other people, then a good principle is to ask how can I unblock them? and how can I make it easy for them to do their work? Raising capital is no exception. Appreciate that people on the other side have a process they must run, think about the boxes they have to check, and make that easy for them. By contrast, going with unorthodox presentation/data formats, insisting on doing the process your way, or pitching your company such that it raises many questions that are hard to answer, are good ways to get shuffled to the bottom of the priority list. The best thing that you can do for busy people is to help them be efficient with their time.

If you’re thinking about putting together a deck for something: good luck! I hope these notes are helpful. If you ever want a second pair of eyes, I’m happy to help. You can reach me at contact@johnloeber.com.

Thanks to Mike and Evan for their feedback and comments on this piece.

Internal investment memos are very different from the public-facing “why we invested” blog posts that many firms tend to write. Some firms will voluntarily publish their memos, but note that these tend to be redacted/modified versions. For example, you may notice that in many of the memos I’ve linked to, details around round pricing and structure tend to be light.

And in turn, they may be expected by their LPs to present this information, etc. Expectations for information cascade all the way throughout the stack, and even if you’re able to persuade someone at one level of the stack that the information doesn’t matter, the next person one level up in the stack will be puzzled why it’s missing. That’s not good!

You could even put a slide of customer reference contact details to call/email in an appendix.